Loan Calculation Detailed Guide

Loan calculation or loan planning is a very important financial skill that every person should understand before applying for any type of loan. Many people take loans for education, housing, vehicles, business, and even daily needs without understanding how repayment works. When you do not understand loan calculation, you often agree to terms that later become a burden. This happens because the total repayment amount becomes much higher than the amount you originally borrowed.

In this complete guide, you will learn every important part of loan calculation or loan planning in simple language. This article is written in a natural, human tone that connects with readers and also helps increase your earnings through high-value financial keywords. Lenders, banks, and financial services pay very high amounts for clicks on loan-related searches. So this type of content helps with earning even if your website traffic is small.

Let us begin with the fundamental understanding of what a loan actually is.

What Is a Loan? Why Do People Take Loans?

A loan is an amount of money provided by a lender to a borrower. The borrower agrees to repay the loan within a specific time period along with an additional cost known as interest. People take loans for many purposes. Some common reasons include:

Purchase of a home

Purchase of a car

Education-related fees

Medical emergencies

Business expansion

Debt consolidation

Daily use expenses in tough situations

A loan can be very helpful when used responsibly. However, it can also create financial stress if you do not understand loan calculation or loan terms properly. The best way to protect yourself from debt pressure is to learn exactly how repayment works.

Why Loan Calculation Should Be Done Before Applying?

Loan calculation or loan planning is the process of understanding how much you will pay in total, including principal, interest, processing fees, and any other charges. Most people focus only on the monthly installment. While the installment is important, the total amount you pay in the end is more important.

Loan calculation helps you understand the complete cost. If you calculate properly, you will be able to compare lenders and choose the one that offers the lowest cost. You will also know whether the loan fits your financial condition.

Without loan calculation, borrowers often make wrong choices. They select long-tenure plans because the installment feels comfortable. But the total repayment becomes very high due to more interest months. This is why every expert advises calculating the loan before signing any agreement.

Important Words Used in Loan Calculation

There are several financial terms involved in loan calculation or loan repayment. Understanding these terms helps you read loan documents with confidence.

Principal Amount

The actual amount you borrow.

Interest Rate

The cost charged by the lender for giving you the loan.

Loan Tenure

The total time you get to repay the loan.

EMI

The monthly installment that you pay.

Processing Fee

A charge taken by the lender for approving the loan.

Total Repayment

The complete amount you will pay, which includes principal plus interest.

Pre-Payment

Paying a part of the loan before the agreed schedule.

Foreclosure

Paying the entire loan amount before the end of the tenure.

Each of these terms directly affects your loan calculation.

How Lenders Calculate Loan Installments?

Lenders use a special mathematical formula to calculate monthly installments. While the formula may look difficult, the idea behind it is simple. Lenders calculate the interest on the principal amount, add that interest to the total repayment, and then divide the repayment into equal installments.

The factors that decide your EMI are:

The money you borrow

The interest rate

The time you choose for repayment

Even a small difference in interest rate can change your EMI. This is the reason loan calculation is so important.

Different Types of Loans and Their Calculation

Loan calculation works similarly for most types of loans. However, interest rates can be different for each type of loan because of lender risk and loan purpose.

Personal Loan

Usually has higher interest because no security is required.

Home Loan

Has lower interest because the property works as security.

Car Loan

Moderate interest and fixed tenure.

Business Loan

Interest varies depending on business income and stability.

Education Loan

Often has lower rates and flexible repayment.

Agriculture Loan

Made for farming needs, with special benefits in some countries.

Online Instant Loan

Easy approval but higher interest due to short tenure.

Each loan uses the same calculation steps, but the interest and fees change. Always compare before finalizing.

Fixed Interest Loan vs. Variable Interest Loan

Understanding these two types will help you choose better.

Fixed Interest Loan

The interest stays the same from beginning to end. Your EMI does not change. Good for financial stability.

Variable Interest Loan

The interest rate can change based on market conditions. EMI may rise or fall. Suitable for people who can handle risk.

Most beginners prefer fixed interest loans because they are simple and predictable.

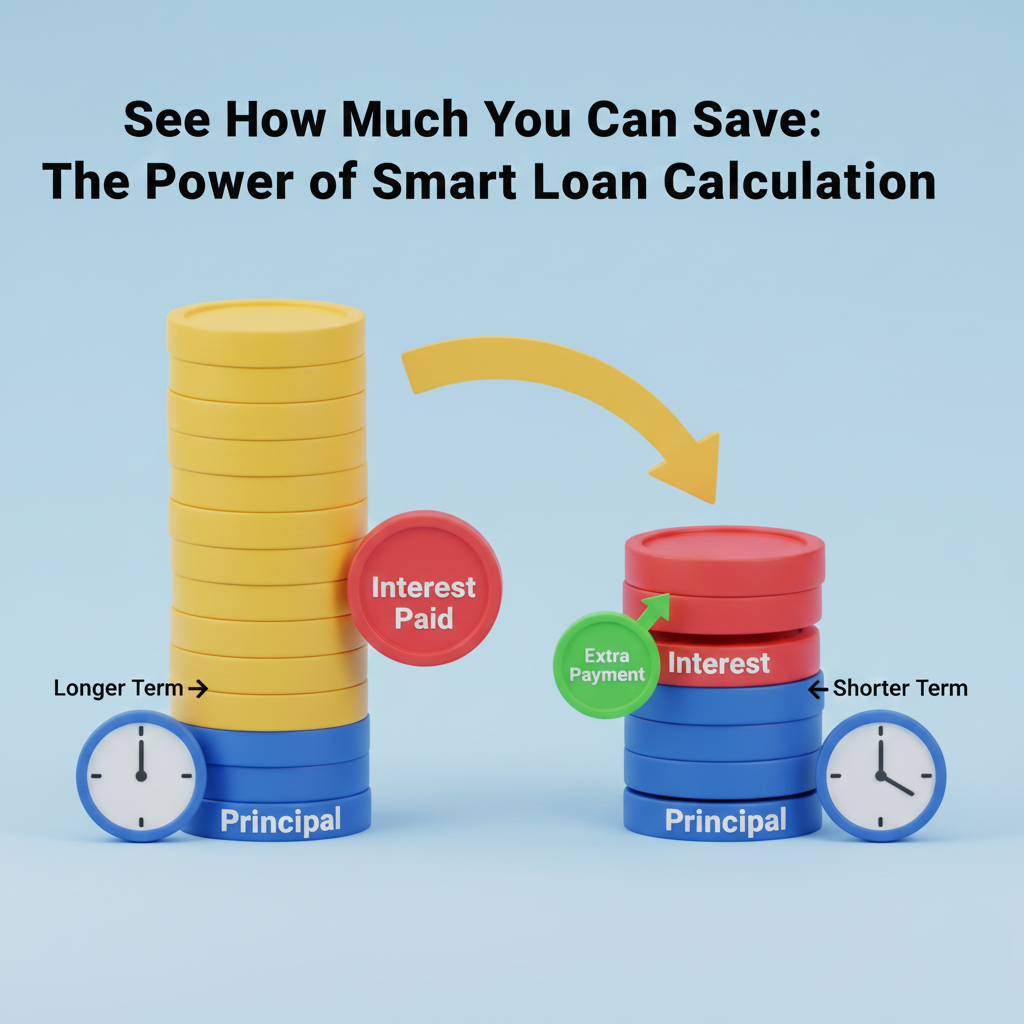

How Interest Rate Changes the Total Cost?

Interest rate is the most important factor in loan calculation. Even a one-percent difference can change the final repayment by a large amount.

Example:

A loan with twelve percent interest is always more expensive than a loan with eight percent interest.

A five-year loan will always cost more than a two-year loan because a longer time means more months of interest.Always aim for a lower interest rate or shorter tenure if possible.

Benefits of Doing Loan Calculation Yourself

Loan calculation gives you several benefits:

You understand how much you must pay.

You avoid hidden costs.

You choose the lender that saves you money.

You plan your budget better.

You avoid unnecessary loans.

You reduce financial stress.

When you calculate everything yourself, you gain control over your financial decisions instead of depending on others.

Common Loan Mistakes That People Make

Many borrowers make simple mistakes that cost them extra money. Some common mistakes are:

Borrowing more money than needed

Ignoring processing fees and other charges

Accepting the first loan offer without comparing

Focusing only on EMI and ignoring total repayment

Not checking late fee charges

Not asking about pre-payment charges

Choosing a long tenure to get a smaller EMI

Avoiding these mistakes can save you a large amount in the long run.

How to Select the Best Loan for Your Needs?

Choosing the right loan is easy if you follow these steps:

Know the exact amount you need.

Check interest rates from multiple lenders.

Calculate the EMI of each option.

Compare total repayment, not just EMI.

Check additional fees.

Read the contract carefully.

Choose the lender with the lowest total cost.

Smart selection saves money every time.

Factors That Affect Your Loan Approval

When you apply for a loan, the lender checks several things before approving it. These include:

Your credit score

Your income level

Your employment status

Your repayment history

Your existing loans

Your financial stability

The better these factors are, the lower the interest rate you receive.

Loan Calculation Helps You Save Money

If you know how to calculate loans, you can avoid costly mistakes. You can save money using these techniques:

Choose a shorter tenure if possible.

Pay extra amounts whenever you have savings.

Avoid late payments.

Improve your credit score.

Avoid taking loans without need.

Compare lenders and negotiate rates.

Even small changes in your loan planning can save you a lot of money.

Loan Calculation for Business Purposes

Business loans require even more careful planning because the amount is usually large and the tenure long. Business owners must calculate repayment before applying. A wrong business loan can affect profit, cash flow, and growth. Use loan calculation to check whether your business income can handle the installments comfortably.

Why Loan Related Articles Earn High CPC and High RPM?

Finance content especially loan and credit-related topics has very high competition among advertisers. Banks, lenders, credit services, and insurance companies all bid high amounts to get customer attention. This means even with low visitors, you can earn good CPC and RPM.

People searching for loan calculation or loan information are usually ready to apply for a loan. Advertisers know this and pay more to reach them. That is why finance keywords are some of the highest-paying keywords in the world.

Loan Calculation Tools and Online Calculators

There are many easy to use online calculators that show your EMI instantly. You only need to enter the principal, interest rate, and tenure. The tool calculates the installment, total interest, and total repayment. These calculators save time and help beginners understand the repayment pattern clearly.

Can You Repay a Loan Early?

Yes, most lenders allow early repayment. Early repayment reduces the interest you pay and helps you become debt-free faster. However, some lenders charge a small fee for early repayment. Always check this rule before signing the loan contract.

How to Avoid Loan Pressure and Debt Stress?

Loan pressure happens when borrowers take more loan than they can handle. You can avoid this pressure by following simple steps:

Calculate your monthly income

Make sure EMI does not exceed thirty percent of your income

Avoid taking multiple loans

Build an emergency fund

Choose loans responsibly

Avoid emotional decisions while borrowing money

Good planning keeps your financial life stable.

Loan Calculation and Financial Discipline

Loan calculation teaches you financial discipline. It makes you more careful about spending, borrowing, and saving. When you understand the true cost of borrowing, you develop better control over your money. This discipline helps you throughout your life.